Gearing up to crack the FRM Exam? Master all types of frm practice questions! Think of them as your personal guide through this complex world of financial risk management. And the more you practice, the more that you get accustomed-not just to the format of the exam, but also to the tricky concepts that come your way. You will not only strengthen your knowledge by diving deep into question types but also sharpen your test-taking strategies. Read along to find out more about what is covered in practice questions and some examples of questions from Zell Education’s exclusively created mock tests!

What Should you do in Terms of FRM Practice Questions?

Attempt questions from official FRM material, third-party providers, and past papers. Spread your practice sessions, focusing on the quality of the questions rather than the quantity. It’s not about solving thousands of questions but knowing the concepts behind the questions. Review and analyze your mistakes regularly to understand knowledge gaps. Early and consistent practice will give you the confidence and familiarity you need to perform to the best of your ability on exam day.

FRM Topics Covered in Practice Questions?

FRM Part I focuses on the basics of risk management, including quantitative analysis, financial markets, and valuation models. Part II gets deeper into the more practical aspects: market, credit, and operational risk management. Each part requires clarity about the essential formulae, models, and natural financial risk scenarios. Questions on all these topics help one get comfortable with the wide range of subjects tested in this exam.

FRM Pass Rate

The FRM is considered one of those tough exams, where the passing rate in Part I usually ranges around 40-50% and a little higher for Part II, around 50-60%. The passing rate indicates the challenge but, in essence, it underlines that one has to prepare seriously and tactically for the exam. Focus your efforts on gaining a conceptual understanding of the core topics and developing test-taking skills to complete the exam on time.

FRM Part 1 Passing Score

While no fixed minimum passing score is there, it is usually advisable to score 55% or higher in Part I. That way you would have a strong chance of mastering the core concepts in all areas. Also, since the examination is based on a percentile score, the higher the score the better your pass chances are in comparison with other candidates.

FRM Part 2 Passing Score

The passing score for Part 2 is around 50-60%. This part tests your application skills concerning the tools to manage risk in real situations; therefore, you should focus on application-oriented questions to score well. Comprehension of complex cases and scenarios is a prerequisite for adequate performance in this part of the test.

FRM Practice Questions: How to Use Them Effectively

Diversify your sources: Practice with material provided by GARP but also connect to coaching classes like Zell Education to have better access to mock tests and practice papers.

Start Early: The earlier you start, the more time you will have to spot your strengths and weaknesses and try to improve on them.

Analyze your performance: Go through your mistakes after every session and put more effort towards your weak areas.

Take Notes: Jot down key concepts and formulas that would be helpful during quick revision.

Imitate the test setting: Practice under timed conditions to get comfortable with pacing and examination pressure.

FRM Exam Sample Questions: Part 1

1. Name one of the following risk metrics that measure the risk as downside deviation instead of standard deviation?

- Treynor ratio

- Sharpe ratio

- Sortino ratio

- Jensen measure

The correct answer is 3.

Explanation: The Sortino ratio uses the downside deviation to measure its risk. This addresses the problem of using standard deviation used by other risk measures since upside volatility is beneficial to investors.

2. Consider the following statements regarding closed-end mutual funds:

- The funds offer investors professional management

- Shares at times trade at a discount to the NAV

- Shares at times trade at premium to the NAV

- Funds are redeemed at their NAVs

Which of the statements above is/are incorrect?

- IV only

- II and III only

- II, III, and IV

- All of the above

The correct answer is 1.

Explanation: Shares of closed-end mutual funds are redeemed at their prevailing market values, not at their NAVs.

All other statements are correct. Shares at times trade at a discount or a premium from the NAV, and these funds offer investors professional management.

3. Blackoil Inc. is an American oil-producing company that sells oil futures to lessen the risk of fluctuating oil prices. This activity can be described as:

- Speculating

- Hedging

- Clearing

- None of the above

The correct answer is 2.

Explanation: Futures contracts are one of the most common derivatives used to hedge risk. Hedgers enter into futures contracts to reduce the price risk of underlying assets. Hedging is an attempt to “lock-in” the value of an asset and hence guarantee a certain level of return to the investor.

4. A trader purchased a European call option on the stock of KKL with a strike price of USD 29.50, and at the same time, sold a European call option on the same stock with a strike price of USD 34.89. Suppose that the final price of the stocks at expiration is USD 44, what are the name and the payoff of the strategy? Ignore the cost of the strategy.

- Name of the strategy: Bear call spread; Payoff: USD -9.15

- Name of the strategy: Bull call spread; Payoff: USD 9.11

- Name of the strategy: Bear call spread; Payoff: USD -5.39

- Name of the strategy: Bull call spread; Payoff: USD 5.39

The correct answer is 4.

Explanation: In a bull spread strategy, an investor buys European call options with a specific strike price (USD 29.50) and simultaneously sells European call options with a higher strike price (USD 34.89).

If the current price (USD 44) is higher than the strike price of the short call option (USD 32), both call options will be exercised, and the payoff of the investor will be X2-X1 or USD 34.89USD 29.50 = USD 5.39.

5. There are some key similarities between the 2007-2009 crisis and the previous crises. In all those crises, there were:

- Notable increases in public debt

- Positive current account balances

- Excessive borrowing from governments and foreign institutions

- House price run-ups

- I and IV

- I, III, and IV

- II, III, and IV

- All of the above

The correct answer is 2.

Explanation: Post-2008-2009 crisis research and analysis have established that the financial crisis was “not special,” but was, in fact, reminiscent of prior crises. In particular, there are important similarities between the 2007-2009 crisis and the previous crises. In the crises mentioned above, there were (IV) house price run-ups, (I) noteworthy increases in public debt, and (III) impurdent borrowing from foreign institutions and governments, (II) triggering negative current account balances.

6. Pick one of the following that best defines a nonrecourse loan?

- A type of loan secured by collateral in which the issuer can seize the collateral but cannot seek from the borrower any further compensation if the borrower defaults.

- A type of loan that is unsecured in which the issuer cannot seek out the borrower for any compensation if the borrower defaults.

- A type of loan secured by collateral, usually a property, in which the issuer can only seek further compensation in the event the collateral does not cover the full value of the defaulted amount.

- A type of loan that is unsecured in which the borrower pays a very low initial interest rate that increases after a few years.

The correct answer is 1.

Explanation: Non-recourse debt is a type of loan secured by collateral, which is usually a property. If the borrower defaults, the issuer can seize the collateral but cannot seek further compensation from the borrower, even if the collateral does not cover the full value of the defaulted amount.

In the lead-up to the financial crisis of 2007-2008, many non-recourse mortgages allowed the lender only to take possession of the borrower’s home. When the housing prices fell, the borrowers sold their homes to the lender for the principal outstanding on the mortgage because the collateral did not cover the full value of the defaulted amount.

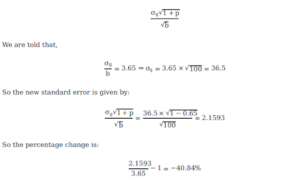

7. The estimated standard error for a Monte Carlo simulation without antithetic variables is 3.65. The antithetic variables are now included so that the correlation between the pairs is -0.65 and the simulation is repeated 100 times. What is the percentage change in standard error?

- 45.65%

- -46.45%

- 40.84%

- -40.84%

The correct answer is 4.

Explanation: Recall that the standard error of the simulation when antithetic variables are included expectation is given by:

8. Pick one of the following statements that inappropriately defines the elements of Enterprise Risk Management (ERM)?

- Stakeholders management refers to sharing or communicating information regarding a firm’s internal risk management processes to external stakeholders.

- Data technology and resources allude to the management of activities that are directly connected to the production of products and services of the firm.

- I only

- II only

- Both I & II

- None of the above

The correct answer is 2.

Explanation: Point I is accurate. Stakeholder management refers to sharing or communicating the information regarding a firm’s internal risk management process to external stakeholders, i.e., shareholders, creditors, regulators, and the public.

Statement II is inaccurate because the “Data technology and resources” element of ERM refers to the improvement of the quality and technology of data used in the evaluation of risks.

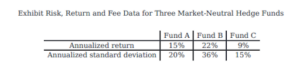

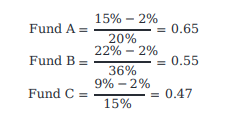

The exhibit below summarizes the risk and return for three market-neutral hedge funds in Canada:

If the risk-free rate in Canada is 2%, which of these funds is most appropriate from an investment perspective, according to the Sharpe ratio?

- Fund A

- Fund B

- Fund C

- Insufficient information

The correct answer is 1.

Explanation: To determine which fund is most appropriate for investment, the Sharpe ratio of the three funds is calculated as follows:

Fund A has the highest Sharpe ratio, which means that it will intensify risk-adjusted performance. As a result, it is most suitable from an investment perspective.

FRM Exam Sample Questions: Part 2

1. Among the natural disasters that have affected the United States over the years, Hurricane Andrew, which hit Florida and Louisiana on August 24, 1992, was the most costly disaster in terms of insurance payouts to those whose houses, vehicles, and businesses were damaged. Approximately $15.5 billion worth of insurance claims were paid at the time. The leading insurers responded by charging higher premiums for coverage. The insurers’ actions are examples of:

- Financial mitigates

- Financial amplifiers

- Stranded assets

- Proactive actions

The correct answer is 1.

The purpose of financial mitigates is to reduce an institution’s exposure to financial risks through proactive and reactive actions. Pre-emptive actions would amount to the banks acting in advance to reduce their vulnerability to the risk factors arising out of climate change. Typical examples could be diversification and strategic asset allocations. A bank would increase investment in sustainable companies that have embraced less carbon-intensive business practices and technology.

Reactive actions would be those responses already taken to the climate risk embedded in a balance sheet exposure. Those include insurance and reinsurance, hedging and securitization, or asset sale which provide the immediate way to lighten a bank’s asset holdings of particularly high-risk assets. Increasing the cost of insurance is an example of reactive financial mitigant.

2. Which of the following statements correctly describes a significant challenge that organizations face in AI risk management?

- The need to eliminate all AI risks before deployment.

- Opacity of AI systems and reliance on third-party components.

- Ensuring that AI systems only function in pre-defined, controlled environments.

- Avoiding any updates or changes to AI systems post-deployment.

The answer is 2.

A is incorrect because the complete elimination of all risks before deployment is impractical and unrealistic in the context of AI, where some level of risk is inherent and often needs to be managed rather than fully eliminated.

C is incorrect because expecting AI systems to only function in pre-defined, controlled environments is not feasible in real-world applications, where AI systems often encounter unpredictable variables and scenarios.

D is incorrect because avoiding updates or changes post-deployment is not practical for AI systems. Continuous improvement and adaptation are often necessary to address evolving risks and changing environments.

3. As part of a complex credit risk management strategy, a financial risk manager needs to explain the distinction between structural and reduced-form models in the context of default correlation models. Which of the following statements accurately describes a feature that differentiates these model types?

- Structural models focus on the legal framework of default, whereas reduced-form models are based on underlying economic factors that impact a firm’s assets.

- Reduced-form models directly specify default correlation based on asset value, while structural models use statistical concepts like copulas to model dependency structures. C. Structural models are based on underlying economic factors that impact a firm’s assets, with default probability correlated through these factors, while reduced-form models directly specify default correlation without linking to the assets’ value.

- Reduced-form models determine default correlation through the common influences on a portfolio, such as market or sector trends, and structural models do not consider systemic factors.

The correct answer is 3.

Structural models for default correlation are founded on the economic factors influencing a firm’s asset values, and they correlate the likelihood of default based on these influences. Contrastingly, reduced-form models bypass the link to the firm’s asset values, directly specifying the default correlation. These models use concepts like copulas to capture complex dependency structures between defaults that go beyond simple linear correlations.

4. Since it was founded ten years ago, Bright Technologies pays no dividends to shareholders and is financed with 100% equity. Recently, management decided to have the firm leveraged and issued a zero-coupon bond with a principal amount of $100 million maturing in exactly three years. If the value of the firm at maturity is $80 million, determine the values of the different components of the firm’s capital structure at the maturity date of the bond.

- Value of equity = $0; value of debt = $80 million

- Value of equity = $20 million; value of debt = $80

- Value of equity = $180 million; value of debt = $100 million

- D.Value of equity = $20 million; value of debt = $0

The correct answer is 1.

Value of equity is the value of a call on the value of the firm with an exercise price which is equal to the face value of the zero-coupon bond, ST = Max(VT – F, 0) = Max(80 – 100, 0) = 0

This implies that equity has no value.

The value of debt is DT = F – Max(F – VT, 0) = 100 – 20 = $80 million

5. John, the Chief Risk Officer of Omega Bank, is implementing a new risk control system. As part of this system, he introduces Key Risk Indicators (KRIS) and Key Control Indicators (KCIs) to monitor risk levels and control effectiveness, respectively. However, some of his team members are confused about the differences between these two types of indicators. Which of the following statements best differentiates between KRIS and KCIS?

- Both KRIS and KCIs measure the potential risks that may impact the achievement of strategic objectives.

- KCIS identifies potential risks, while KRIS measures the effectiveness of control mechanisms in mitigating those risks.

- Both KRIS and KCIS monitor the effectiveness of risk control mechanisms.

- KRIS identifies potential risks that may hinder the achievement of an objective, while KCIS measures the effectiveness of mitigation mechanisms.

The answer is 4.

KRIS (Key Risk Indicators) are used to identify and signal increasing risks that may hinder the achievement of an objective. On the other hand, KCIS (Key Control Indicators) is designed to measure the effectiveness of control mechanisms in mitigating those risks.

6. Jainish Sheth, a market analyst at Smart Investment Bank, has been tasked with the development of early warning signals to help the bank monitor potential liquidity stress events. At the preliminary stage, Mr. Sheth has researched a set of background guidelines as follows:

- All EWIS must be updated every two months to detect potentially threatening events.

- Their bank should conduct a variety of short-term and protracted bank-specific and market-wide liquidity stress tests using conservative and regularly reviewed assumptions.

- The bank should establish a robust escalation policy so that critical decisions and transactions are handled at an appropriate level of management.

As a risk analyst, which of the above proposals would you disagree with?

- a

- b

- c

- None of the above

The correct answer is 1.

An indicator that has not been updated for more than a month is unlikely to satisfy the early aspect of the EWI. In practice, EWIS are updated daily, weekly or monthly.

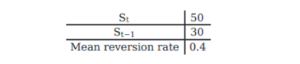

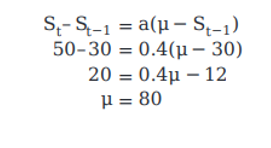

7. Given the following data above a variable S:

What is the long-run mean value for the variable?

- 60

- 80

- 100

- 75

The correct answer is 2.

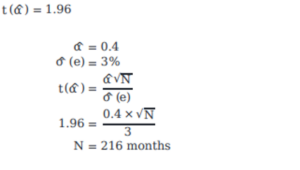

8. The given portfolio has an alpha of 0.4 and a standard deviation for the nonsystematic risk per month equal to 3. What is the value of N at a 95% level of significance?

- 4 months

- 14 months

- 108 months

- 216 months

The correct answer is 4.

At the 95% significance level,

9. The following information has been extracted from the P&L of a European Bank over 3 years:

Using the Standardized Measurement Approach, the bank’s Business indicator (BI) for the year ended 31 Dec 20X9 is closest to:

- 4 billion

- 5 billion

- 3.2 billion

- 500 million

The correct answer is 2.

Under the standardized measurement approach, SMA, a bank’s BI has three components: the interest, leases, and dividends component (ILDC), the services component (SC), and the financial component, FC. To determine the value of BI, we must sum the average over three years: t, t – 1 and t – 2,

How Can Zell Education Help You Prepare for the FRM Exam Paper?

With expert-led classes, updated study materials, and personalized coaching, comprehensive FRM certification is provided by Zell Education. They help students with detailed guidance on core topics, tackle hard concepts, and provide a sufficient number of practice questions for the FRM syllabus details. Besides that, Zell Education encourages their students to take mock exams and provide feedback sessions for the students to cope well with the complexity and format of the exam. Individualized training boosts the level of confidence and assures better preparation for the exam.

FAQ’s on FRM Practice Questions

Are FRM practice questions tough?

Yes, FRM practice questions can be challenging to work through. They do indeed mirror the complexity of the exam itself. Many of them will require a deep conceptual understanding of financial risk management and an ability to apply concepts to the real world.

How can I practice for the FRM exam?

You do practice through materials provided by GARP, mock tests, and practice papers. The key is to first go through all the core topics and practice them in a timed simulation environment.

Is 4 months enough for FRM level 1?

Yes, 4 months may be sufficient, given one spends 15-20 hours of focused studying every week. Additionally, you will need to put in time for practice questions and reviews of core concepts.

Are GARP books enough for FRM?

GARP books cover the FRM syllabus comprehensively; however, studying practice papers and mock exams helps candidates prepare for the format and difficulty level of the exam.

Why Zell?

- • Largest Provider for Global F&A Courses

- • 4.6 Google Review Rating

- • 1000+ Global Placement Partners

- • Placement Opportunities at the Big 4

- • 100+ Global & Indian Rank Holders

- • 100+ Faculty Network

- • 10,000+ Students Placed

Speak to A Career Counselor

Zell's 10th Anniversary Offer - Avail a 10% Scholarship