Imagine, you’re the decision-maker in a bustling company, and it’s finally time to make some significant financial decisions! Invest in that cutting-edge new technology or expand operations? That’s when capital budgeting enters to be your guiding compass.

Capital budgeting is the strategic process undertaken by companies to evaluate and prioritize significant investments. Every dollar spent has the potential to generate high returns. Capital Budgeting is screening for potential projects. Through the study of cash inflow and outflow over various periods to make sound decisions.

Capital budgeting goes beyond creating the financial future of the organization, it outlines direction for long-term growth. Is it time to unleash the secrets behind this process and why it matters? Read along to find out!

What is Capital Budgeting?

Capital budgeting is a process by which businesses analyze and pick long-term investments that align with their strategic targets. It investigates whether a specific project or expenditure would be sensible and profitable. Examples of capital budget decisions include buying new equipment, new products, new firms, and even building a new facility. The objective of sponsoring projects would be the greatest returns with potential value to the firm.

How does Capital Budgeting Work?

Capital budgeting involves a whole series of well-structured steps meant to make an informed decision:

Identify Potential Investments: This is a generative step for ideas of potential projects or investments. These might be generated from some market research, strategic planning sessions, or even just through everyday operational needs.

Estimating Cash Flows: After the initial projects are chosen, there would be cash inflows and outflows on each investment to be incurred. These range from the initial costs, running expenses, expected revenues, and salvage values at the end of the project’s life.

Evaluation of Investment Options: Several capital budgeting techniques are employed in evaluating the selected projects. Amongst these more often applied techniques are:

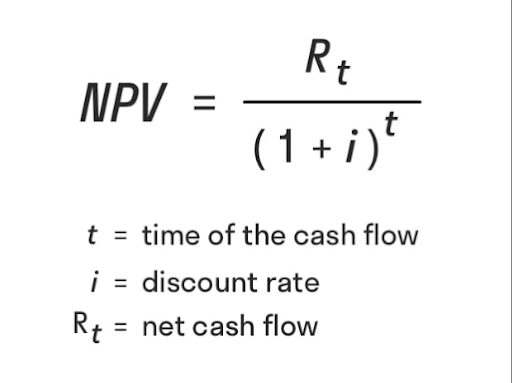

- Net Present Value (NPV): The difference between the present values of inflows and outflows for knowing whether there is a positive payback from the investment or not.

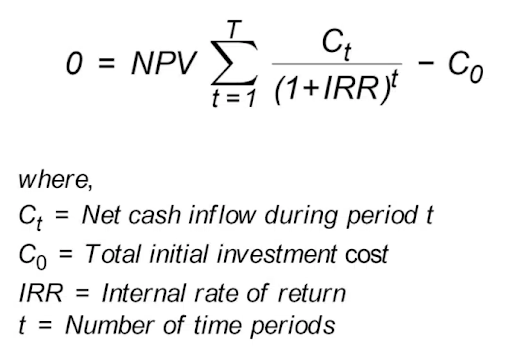

- Internal Rate of Return (IRR): The discount rate at which the net present value of cash flows becomes zero. It uses this to determine how profitable the project can potentially be.

- Payback Period: It determines how long it will take for the initial investment to be recovered based on cash inflows.

- Profitability Index (PI): The profitability index measures the ratio of the present value of cash inflows to the initial investment, indicating the value generated per unit of investment.

Make the Decision: After analyzing the prospective investments with selected methods of evaluation, management then decides which projects to undertake based on their strategic fit, risk capacity, and access to funds.

Monitoring and Review: Once a decision has been made to invest in a particular project, it becomes necessary to track the actual execution of the project against the expected projection. Periodic reviews reveal deviations from expectations, allowing for timely corrections if necessary.

Importance of Capital Budgeting

Capital budgeting is vital for the following reasons:

- Resource Allocation: Capital budgeting would ensure optimal utilization of capital since it would help companies allocate their limited resources to the most promising projects.

- Risk Management: Capital budgeting helps evaluate investments for potential returns and associated risks, thus mitigating financial risks on a business.

- Strategic Planning: Capital budgeting optimizes the strategy since investment decisions are within the context of the company’s long-term strategic goals, with projects showing total contribution to growth and profitability.

- Performance Measurement: The performance of a company can be measured, inadequacies in areas of concern are identified, and further decisions about capital investments can be improved through periodic tracking and evaluation of capital projects.

- Financial Health: Proper capital budgeting will contribute to the financial soundness of a firm because investments yield appropriate returns that cover costs and support the continuation of current operations.

Features of Capital Budgeting

The following are some of the features of capital budgeting:

Long-Term Focus: A capital budgeting decision typically creates a long-term investment that requires huge capital expenditures spread over several years. In this regard, the company should consider any project with viable long-term profitability.

Cash Flow Analysis: The technique centers on estimating future cash flows (inflows and outflows) related to any project instead of accounting for profits, giving a clearer view of whether or not the project is financially viable.

Risk Analysis: In capital budgeting, risks associated with probable investments are evaluated such that uncertainties that might either make or break the project can be identified.

Time Value of Money: It allows for the application of the time value of money since cash flows at a particular future date are considered to have less value as opposed to the same amount of cash today.

Financial Evaluation Techniques: The process involves the use of financial evaluation techniques such as NPV, and IRR to assess the net profitability of a project and the decision-making process.

Budget Constraints: Capital budgeting recognizes the fact that firms have limited capital and that projects are prioritized based on their potential return.

Objectives of Capital Budgeting

The following are some of the objectives of capital budgeting:

- Maximize Profits: The goal is to identify projects that give the greatest returns to maximize the firm’s profits.

- Ensure Strategic Aims: Capital budgeting aims at ensuring investments in ways that facilitate the achievement of the strategic vision of the firm.

- Efficient Usage of Resources: It aims to provide a suitable allocation of financial resources to different projects to achieve maximum resource usage with minimum wastage.

- Risk Minimization: The capital budgeting study of possible risks strives to shield the firm from financial risks and raise the level of stability in the organization.

- Capital Budgeting Process: The process helps in predicting the cash-flow requirements that enable proper financial planning for capital structure management of the company.

Capital Budgeting Methods

1. Net Present Value (NPV)

Example: If an investment of $100,000 is expected to pay back $30,000 annually over five years with a discount rate of 10%, the net present value is calculated to determine whether it should be accepted or not.

2. Internal Rate of Return (IRR)

Example: For the same investment scenario as above, you would calculate the IRR to see if it exceeds your required return rate.

3. Payback Period

Example: If a project costs $200,000 and generates $50,000 annually, then calculate the payback period.

4. Profitability Index (PI)

Example: If the present value of cash inflows from a project is $250,000, and the initial investment is $100,000, then calculate the profitability index.

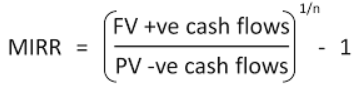

5. Modified Internal Rate of Return (MIRR)

Example: The MIRR can provide a more accurate picture than the IRR when cash inflows are reinvested at a different rate than the project’s IRR.

Types of Capital Budgeting

Budgets can take various forms, such as incremental, activity-based, value proposition, or zero-based. While zero-based budgets start from scratch, incremental or activity-based budgets may build upon a prior-year budget to establish a baseline. When it comes to the process of capital budgeting, any of these methods can be employed, but zero-based budgets are particularly suitable for new projects.

Capital budgeting can be classified into many types based on different criteria. Some of them are:

Based on the Nature of the Investment:

- Replacement Projects: These are investments that have been undertaken so that the replacement of old or obsolete equipment will be done to sustain operational efficiency.

- Expansion Projects: These are investments made with the primary intention of expanding the capacity or scope of the business, for instance, opening new facilities or the increasing number of production lines.

- New Projects: The expenses are undertaken on entirely new initiatives, products, or services that the organization has not undertaken in the past.

Based on the Duration:

- Short-Term Capital Budgeting: All those investments that have the potential to pay back within one year or less are considered short-term and relate to direct operating needs.

- Long-Term Capital Budgeting: These are the projects that take more than one year to repay. Infrastructural development and major expansions are involved.

Based on Risk:

- High-Risk Capital Budgeting: Investments that carry a possibility of higher returns, but also a higher risk of loss such as in speculative ventures.

- Low-Risk Capital Budgeting: These investments result in lesser returns but also bring in lower risk; for example stable projects or established ones.

The Process of Capital Budgeting

Wondering what the process of capital budgeting seems like? Here’s a glimpse into the real picture.

- Identifying the project and creating it: The initial step involved in capital budgeting is to identify the investment opportunities and create a proposal for the same. These projects need to be based on high returns so that the management can approve them on the basis of profitability. These projects could either be an extension of the existing product range or something entirely new.

- Project evaluation and analysis: Based on the company’s short-term and long-term objectives, the project needs to be formulated. While evaluating the project, details of the overall expenditure, time spent and the expected benefits need to be calculated and presented to the management in order to make a sound decision.

- Controlling capital expenditure: While selecting the project based on the revenue is the main objective of capital budgeting, it is not the end. The expenditure still needs to be controlled. The process of capital budgeting ensures that the expenses are further controlled by setting the right budget.

- Searching the right fund sources: The Capital Budgeting Incharge needs to quantify the total expenditure to ensure the funds that need to be borrowed and from where exactly. A balance needs to be created between funds borrowed from different sources and the revenue distribution.

Factors affecting Capital Budgeting

There are a variety of factors influencing the decisions for capital budgeting, including:

Cost of Capital: Higher financing costs (debt vs. equity) push up the hurdle rate, thus making it hard to deliver an adequate return.

Estimates of Cash Flows: The cash flow estimates are highly crucial; exceedingly optimistic or overly conservative projections may mislead investment decisions.

Economic Factors: Interest rates, inflation, and overall market demand create an environment where some projects have more scope than others.

Regulatory Framework: Government policies and regulations sometimes attract investments and sometimes repel them.

Technological Changes: Changes may affect the cost and the feasibility of the project.

Market Competition: At times, an investment may be required to stay competitive within the market.

Management Risk Tolerance: The attitude of the leaders to risk will help determine which projects are selected over and above mere financial measurement.

Capital Budgeting Decisions

Capital budgeting is a decision that depicts how the companies allocate resources for long-term investment. Therefore, the decisions are made on financial analysis based on profitability and risks. Key components include:

- Evaluating Projects: Companies assess and review potential projects in estimating cash flows and returns.

- Prioritization: Projects are ranked considering metrics like NPV, IRR, or payback period.

- Long-Term Focus: Decisions consider not only immediate returns but also meeting long-term strategic direction.

- Risk Assessment: Market conditions, competition, and regulations are evaluated to help manage risk.

- Approval and Funding: The projects are funded through debt, equity, or retained earnings after they are prioritized and approved.

Capital Budgeting Tools

While capital assets are only a small part of the company’s total assets, they still are the ones in line with the organisation’s long-term goals. They are strategically planned in order to generate revenue. Capital budgeting professionals that hope to maximise their revenue are always on the lookout for investment opportunities.

Here are some of the capital budgeting tools used by professionals to prepare a full-proof model:

- Internal rate of return calculation

- Net present value report

- Profitability index

- Accounting rate of return

- Pay period

Limitations of Capital Budgeting

Capital budgeting is a critical process but not without limitations. Here are some common challenges organizations face while making capital budgeting decisions:

Estimation Errors: It is challenging to estimate future cash flows with exact accuracy. Revenues can be overestimated, and costs underestimated, resulting in incorrect decisions to invest.

Ignore Non-Financial Factors: The conventional approaches to capital budgeting focus largely on financial information; the qualitative factors which can include employee satisfaction, environmental impact, or market reputation are often ignored.

Static Analysis: Capital budgeting techniques tend to be static and do not take into consideration changes in market conditions, technological changes, or changes in consumer preferences.

Short-Term Bias: Focus on short payback period projects even though long-term investments may have a higher payback in the long term.

Complex and Resource-Intensive: Capital budgeting is a complex and resource-intensive process, as it involves a vast amount of time and extensive expertise to source the data and to make the analysis.

Rigidity: It becomes difficult to reverse or abandon a project once a decision has been taken on capital budgeting, even when circumstances change.

Deciding on Capital Budgeting

Since the major goal of capital budgeting is increased profitability, the selection of the project is based on maximum revenue or reduced costs. Here’s a glimpse of how most capital budgeting decisions are made.

1. Accept/Reject Decision: Generally the projects that yield a higher return on investment get accepted while the ones that do not seem as profitable often tend to get rejected. Most independent projects get approved, but those competing with one another have a chance of being further shortlisted.

2. Mutually exclusive project decision: As mentioned earlier, competing projects have a chance of being further shortlisted. If there are 5 such proposals submitted at the same time then the acceptance of any type would mean the others get rejected instantly. This is referred to as a mutually exclusive project decision.

3. Capital rationing decision: In a case where a firm has a huge chunk of capital to invest in the projects the proposals submitted at an individual level get accepted quite easily. The rest of the proposals are then rated as per the revenue they might bring in and the acceptance of the proposals depends on the ranking.

Conclusion

Capital budgeting is the most critical process through which organizations can equip themselves to make the best possible long-term investment choices. By analysing projects or alternatives with diverse financial methods, companies can truly optimally allocate resources to boost profitability and achieve strategic objectivity. Effective capital budgeting directly correlates with sustainable growth and the generation of value.

FAQ’s on What Is Capital Budgeting & It’s Process

What is capital budgeting?

Capital budgeting is the process a company undertakes to evaluate and rank major long-term investments, including new projects or purchasing new assets.

What are the techniques of capital budgeting?

The most commonly employed techniques include DCF, Payback Period, NPV, and IRR.

What is a capital budget decision?

A capital budget decision identifies the decision to invest in long-term projects that yield returns in the future such as new equipment and expansion.

What are the types of capital?

The principal categories of capital are debt, equity, and working capital, which businesses utilize for their operations and investments.

What is the formula for capital budgeting?

The one important formula in capital budgeting is the formula of Net Present Value.

What are the five steps of capital budgeting analysis?

The first step of capital budgeting includes exploring new opportunities followed by estimating costs, determining the benefits, assessing any potential risk involved, and making the final decision.

Why Zell?

- • Largest Provider for Global F&A Courses

- • 4.6 Google Review Rating

- • 1000+ Global Placement Partners

- • Placement Opportunities at the Big 4

- • 100+ Global & Indian Rank Holders

- • 100+ Faculty Network

- • 10,000+ Students Placed

Speak to A Career Counselor

Zell's 10th Anniversary Offer - Avail a 10% Scholarship